Posts with tag 'John Yoder Team'

Subscribe and receive email notifications of new blog posts.

RSS Feed

RSS Feed

23

Get Ahead of the 30 Minute Showing!

Get Ahead of the 30 Minute Showing

Back in the days of abundant inventory, buyer used showings as a way to explore whether or not the property was a fit for their needs and goals, and they usually had an hour to do it. Those days are no longer here. In this market, you'll rarely have the opportunity to spend an hour touring a property. Rather, you might receive half an hour, and you may not be the only buyer touring!

Given that you're making such a big decision, and half an hour seems like so little time, I have advice for you.

Consider the showing as a way to confirm, rather than a way to explore. Use the resources available online to determine whether or not a listing is likely to be a fit for you prior to the showing. If the answer is yes, schedule! If the answer is no, don't. I mean it.

This perspective shift could be a breakthrough in your home search, and it ties into previous advice I've given that buyers need to be picky when scheduling showings. To briefly recap, you should determine what the most important goals are for your home search, and stay true to those. This means that if location is most important, and you want to be in a walkable community near downtown Mount Vernon, you don't look at properties in say, Howard. If you're really needing a home with more than 1,500 square feet because your family is expanding, then it's important that you don't spend precious time looking at homes with 1,000 square feet.

So, how can you determine whether or not a listing is likely to be a fit without walking through it?

Well, agents got creative during the pandemic, and starting offering more information about their listings online. This includes more detailed photos (sometimes, even basement and garage photos, or photos of the mechanicals!), and 360 tours where you can essentially walk through the home from the comfort of your couch. It's important that you use these resources, look through all of the photos, watch the video tours, and open the property disclosures if they are available to you. All of these resources are often included in the multiple listing service or agent websites.

Another thing you want to do is look at the location on a map. Figure out how far the property is from your place of work, from shopping and restaurants, etc. Again, your time is precious in this process, and it will just discourage you to drive to a showing only to discover that the location is inconvenient for you.

I promise, all of this work on the front end will be worth it because it will save you time and hassle.

This process will put you a step ahead of other buyers.

It will also provide you the clarity you need in order to do what it takes to win it. That is, if the showing confirms it's a fit!

Isn't this empowering? If I'm getting a sense of one thing from my buyers right now, it's that they feel like they have little control, but that's not always the case. This shift places you back in the driver's seat. These complex market conditions do not have to control your home search if you don't let them.

Until next time,

Cassie Johnson

Key Realty - John Yoder Team

16

Buyers, Be Picky!

Buyers, Be Picky!

This week, the team has some advice for buyers that may seem counterintuitive, but I promise that I am not messing with you!

In this ultra competitive market with very low inventory, it's easy to want to look at every listing that comes up. It's very natural for buyers to want to take a look at homes that don't really meet their criteria "to see" if they can make it work.

We have been recommending a different approach, encouraging buyer to be picky. Hear me out…

If you're considering buying right now, it's extremely important that you decide which criteria is highest priority, and then stay committed to those criteria. Don't know what those criteria may be?

Start by...

9

How Do Agents Price Listings?

How Do Agents Price Listings?

Have you ever been looking at listings online, wondering how the agent and their client came up with the asking price? Well, the process usually involves research and some strategy, and it's rarely arbitrary.

The most common way to chose a list price is to compare the property to be listed with similar properties that have sold recently. Agents will look at the sold price of homes that are similar in square footage, condition, bedrooms and bathrooms, and in the same neighborhood. They'll use those sold prices, often in terms of price per square foot as a base point.

When it comes to sales comparison, there are other relevant factors to look at as well. Days on market will give a glimpse of the market reac...

7

Buy-Then-Sell Strategies That Can Make Your Life Easier in This Market

Buy-Then-Sell Strategies That Can Make Your Life Easier in This Market

Has anyone taken the time to tell you that you may not need to sell before you buy your next home? Our team has had this discussion with our friends and clients, and we've found that many homeowners are delaying their plans to sell because they are afraid of being homeless. This makes complete sense— I wouldn't want to face homelessness either. This market is ultra-competitive, and while drastic home appreciation creates a major opportunity for homeowners, current market conditions present challenges as well.

27

Is the Current Housing Market a Bubble?

Is the Current Housing Market a Bubble?

We've been getting a lot of questions recently about whether or not the current housing market is a bubble and if there's a "Great Recession" type crash around the corner. Our team leader, John Yoder, would like to weigh in on this because some of the messaging out there doesn't really add up. In his opinion, the market is not a bubble, though it is problematic. Keep reading to hear why!

Hi everyone! This is John Yoder with Key Realty – John Yoder Team. I'm excited to discuss this topic because I've experienced some different market cycles in the real estate industry. Like so many Americans, I clearly remember the effects of the 2008 recession in terms of property value. I was an investor during this crisis, and learned a lot through the process. I can say from experience and my research on current market conditions, that this market is different than the market in, say, 2007. Though this market presents many challenges, I don't believe it's a bubble.

For starters, let's talk about why today's market feels like 2007. Some of the similarities are striking. We have dramatic price appreciation. The Case-Schiller home price index released on April 27 this year reported a 12% annual price jump in home values nationally for February 2021 compared with February 2020. Knox County is reporting similar numbers with a 10.4% increase in home values in 2020 as compared with 2019.

Homes are selling over appraised value, at times by tens of thousands of dollars and even more in some markets. We have bidding wars and inventory shortages.

This chart shows how inventory has declined over the last year to levels not seen since the early 2000's:

However, the differences are also striking and that is what we want to focus on today.

While we are seeing inventory shortages similar to the early 2000s a key difference is interest rates.

As you can see from this chart, interest rates in '06 and '07 were in the 5-7% range for a 30 year, fixed rate loan. However, today, those rates are right around 3%. That's a huge difference and makes purchasing extremely attractive right now.

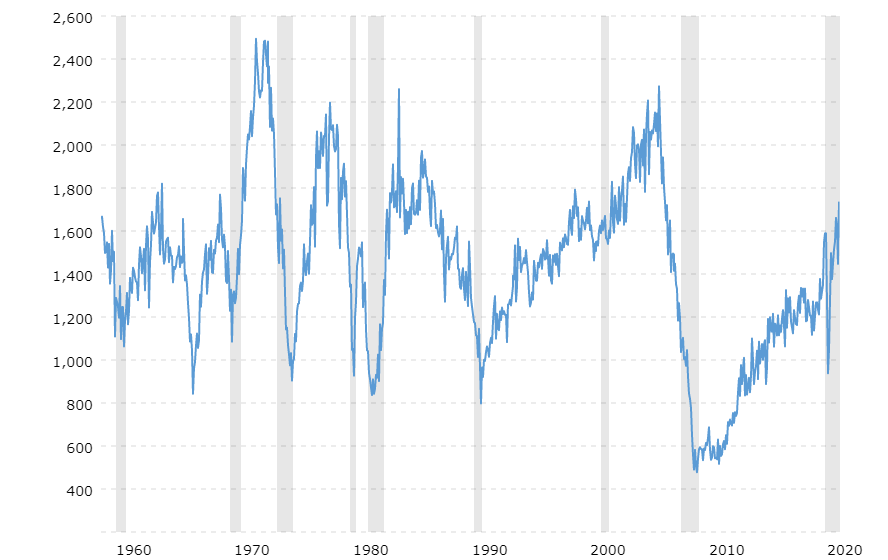

This next chart is one of my favorites and helps to show exactly how we got here in terms of housing inventory:

This chart shows home starts, or new construction, from 1959 to present. You can see that from 1959 through 2007 the US averaged over 1.5 million home starts per year. But from 2008 to present, we averaged less than 1 million home starts per year. That's 13 years of under building.

It took some time to absorb the excess inventory coming out of the recession, but now we're faced with a severe housing shortage that probably won't go away any time soon.

Just how bad is our national housing shortage? Sam Khater, Chief Economist for Freddie Mac wrote in an April 15 article that by their estimates, the US is 3.8 million single family homes short of the inventory needed for a balanced market. That number is up 52% from 2018 when Freddie Mac estimated that the national housing shortage was at 2.5 million units.

This increase is surprising in the context of the pandemic and related economic challenges. According to Khater, "A continued increase in housing shortage is extremely unusual; typically, in a recession, housing demand declines and supply rises."*

So what is driving this shortage? Khater says "The main driver of the housing shortfall has been the long-term decline in the construction of single-family homes."As we noted in the home starts chart earlier, building has not fully recovered since the 2008 recession. Commonly cited factors that contribute to underbuilding are lack of available construction labor, land use regulations, zoning restrictions, NIMBYism (not in my back yard), lack of developers and lack of land to develop.

We have seen that both inventory and interest rates are substantially lower than they were in 2007. What other indicators do we have that today's market is structurally sound?

Let's look at loan underwriting. One of the key factors that led to the 2008 recession was easy credit or "no doc loans." Borrowers were able to purchase with little or no money down and very inadequate underwriting. This was combined with predatory loan products. Payments were affordable at first, but jumped significantly after a few years. Many buyers thought it would be easy to refinance when the time came. But market and economic conditions changed and that wasn't possible for many.

Today, we have much stricter underwriting standards and 30-year fixed-rate loans are the norm. Taylor Marr, leading Economist for real estate website Redfin says it well:

"The key difference now versus during the housing bubble before the Great Recession is that back then it was easy credit that fueled speculation, not cheap credit. It wasn't uncommon for buyers to put nothing down and speculate on real estate because all they had to do was fill out a few pieces of paper and no one cared about the actual numbers. This time around the demand that's fueling appreciating prices is real – from families, newly remote workers, and companies relocating employees to lower tax, lower regulation states."**

So if today's housing market is not a bubble, what is the primary cause for concern?

From my perspective, it's affordability, especially for first time home buyers. The Wall Street Journal reported in a May 19 article that the Federal Reserve is starting to signal an eventual move away from easy money policies which would trigger higher interest rates. Higher rates combined with continued price appreciation will start to price some buyers out of the market.

What should you do if you're looking to buy a home and/or to make a difference in the current market imbalance?

First, talk to a lender early in the process. Be prepared to save for a larger down payment than what you originally anticipated.

Second, consider building if you are in a financial position to do so. Our office keeps an updated list of builders with short waiting time.

Third, support responsible, local development across all price points. We all need to do our part to advocate for a more balanced market. A healthy, balanced market helps everyone and provides housing and financial stability to more individuals and families.

We'd love to hear from you, so please leave your thoughts in a comment below!

John Yoder

Key Realty - John Yoder Team

*Source Freddie Mac, freddiemac.com/perspectives/sam_khater/20210415_single_family_shortage.page?

freddiemac.com/research/insight/20210507_housing_supply.page?

**Source: Wall Street Journal, wsj.com/articles/fed-officials-say-they-are-closely-watching-for-right-moment-to-make-policy-shift-11621445379

Additional information for this video provided by Forbes Magazine, April 2021.forbes.com/sites/petertaylor/2021/04/18/yes-americas-housing-market-is-officially-over-heating-everywhere-how-long-can-it-last/?sh=85b2a0244378

|

|