Posts from May 2021

Subscribe and receive email notifications of new blog posts.

RSS Feed

RSS Feed

27

Is the Current Housing Market a Bubble?

Is the Current Housing Market a Bubble?

We've been getting a lot of questions recently about whether or not the current housing market is a bubble and if there's a "Great Recession" type crash around the corner. Our team leader, John Yoder, would like to weigh in on this because some of the messaging out there doesn't really add up. In his opinion, the market is not a bubble, though it is problematic. Keep reading to hear why!

Hi everyone! This is John Yoder with Key Realty – John Yoder Team. I'm excited to discuss this topic because I've experienced some different market cycles in the real estate industry. Like so many Americans, I clearly remember the effects of the 2008 recession in terms of property value. I was an investor during this crisis, and learned a lot through the process. I can say from experience and my research on current market conditions, that this market is different than the market in, say, 2007. Though this market presents many challenges, I don't believe it's a bubble.

For starters, let's talk about why today's market feels like 2007. Some of the similarities are striking. We have dramatic price appreciation. The Case-Schiller home price index released on April 27 this year reported a 12% annual price jump in home values nationally for February 2021 compared with February 2020. Knox County is reporting similar numbers with a 10.4% increase in home values in 2020 as compared with 2019.

Homes are selling over appraised value, at times by tens of thousands of dollars and even more in some markets. We have bidding wars and inventory shortages.

This chart shows how inventory has declined over the last year to levels not seen since the early 2000's:

However, the differences are also striking and that is what we want to focus on today.

While we are seeing inventory shortages similar to the early 2000s a key difference is interest rates.

As you can see from this chart, interest rates in '06 and '07 were in the 5-7% range for a 30 year, fixed rate loan. However, today, those rates are right around 3%. That's a huge difference and makes purchasing extremely attractive right now.

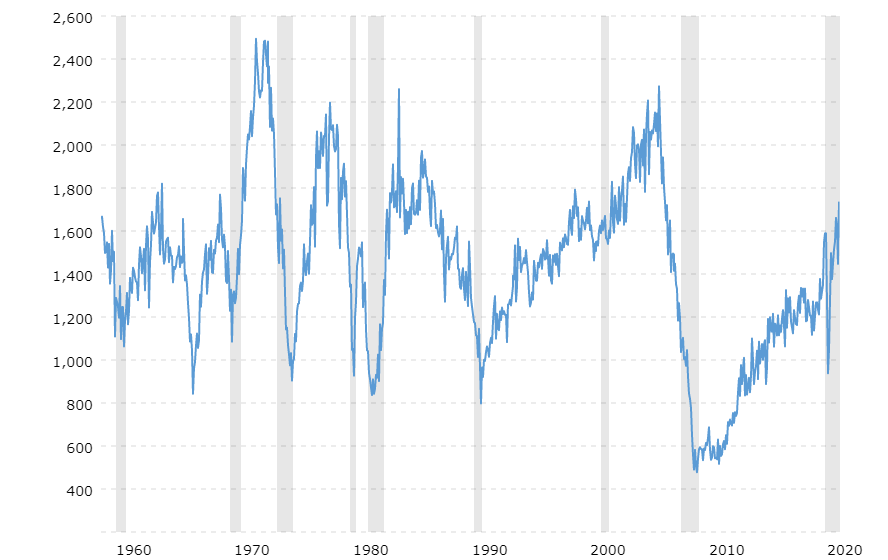

This next chart is one of my favorites and helps to show exactly how we got here in terms of housing inventory:

This chart shows home starts, or new construction, from 1959 to present. You can see that from 1959 through 2007 the US averaged over 1.5 million home starts per year. But from 2008 to present, we averaged less than 1 million home starts per year. That's 13 years of under building.

It took some time to absorb the excess inventory coming out of the recession, but now we're faced with a severe housing shortage that probably won't go away any time soon.

Just how bad is our national housing shortage? Sam Khater, Chief Economist for Freddie Mac wrote in an April 15 article that by their estimates, the US is 3.8 million single family homes short of the inventory needed for a balanced market. That number is up 52% from 2018 when Freddie Mac estimated that the national housing shortage was at 2.5 million units.

This increase is surprising in the context of the pandemic and related economic challenges. According to Khater, "A continued increase in housing shortage is extremely unusual; typically, in a recession, housing demand declines and supply rises."*

So what is driving this shortage? Khater says "The main driver of the housing shortfall has been the long-term decline in the construction of single-family homes."As we noted in the home starts chart earlier, building has not fully recovered since the 2008 recession. Commonly cited factors that contribute to underbuilding are lack of available construction labor, land use regulations, zoning restrictions, NIMBYism (not in my back yard), lack of developers and lack of land to develop.

We have seen that both inventory and interest rates are substantially lower than they were in 2007. What other indicators do we have that today's market is structurally sound?

Let's look at loan underwriting. One of the key factors that led to the 2008 recession was easy credit or "no doc loans." Borrowers were able to purchase with little or no money down and very inadequate underwriting. This was combined with predatory loan products. Payments were affordable at first, but jumped significantly after a few years. Many buyers thought it would be easy to refinance when the time came. But market and economic conditions changed and that wasn't possible for many.

Today, we have much stricter underwriting standards and 30-year fixed-rate loans are the norm. Taylor Marr, leading Economist for real estate website Redfin says it well:

"The key difference now versus during the housing bubble before the Great Recession is that back then it was easy credit that fueled speculation, not cheap credit. It wasn't uncommon for buyers to put nothing down and speculate on real estate because all they had to do was fill out a few pieces of paper and no one cared about the actual numbers. This time around the demand that's fueling appreciating prices is real – from families, newly remote workers, and companies relocating employees to lower tax, lower regulation states."**

So if today's housing market is not a bubble, what is the primary cause for concern?

From my perspective, it's affordability, especially for first time home buyers. The Wall Street Journal reported in a May 19 article that the Federal Reserve is starting to signal an eventual move away from easy money policies which would trigger higher interest rates. Higher rates combined with continued price appreciation will start to price some buyers out of the market.

What should you do if you're looking to buy a home and/or to make a difference in the current market imbalance?

First, talk to a lender early in the process. Be prepared to save for a larger down payment than what you originally anticipated.

Second, consider building if you are in a financial position to do so. Our office keeps an updated list of builders with short waiting time.

Third, support responsible, local development across all price points. We all need to do our part to advocate for a more balanced market. A healthy, balanced market helps everyone and provides housing and financial stability to more individuals and families.

We'd love to hear from you, so please leave your thoughts in a comment below!

John Yoder

Key Realty - John Yoder Team

*Source Freddie Mac, freddiemac.com/perspectives/sam_khater/20210415_single_family_shortage.page?

freddiemac.com/research/insight/20210507_housing_supply.page?

**Source: Wall Street Journal, wsj.com/articles/fed-officials-say-they-are-closely-watching-for-right-moment-to-make-policy-shift-11621445379

Additional information for this video provided by Forbes Magazine, April 2021.forbes.com/sites/petertaylor/2021/04/18/yes-americas-housing-market-is-officially-over-heating-everywhere-how-long-can-it-last/?sh=85b2a0244378

24

How to Know if It's a Good Time for YOU to Sell

How to Know if It's a Good Time for YOU to Sell

Buying and selling in the same market cycle, in the same region, can be tricky and overwhelming. I have this conversation almost daily with my clients, and I've found that the majority of people who are considering selling their home share a common concern: that they don't want to deal with the pressure of buying in a hot seller's market.

First of all, this is completely understandable. It's reasonable -- smart even! -- to wonder what the advantage is to selling in an ultra-competitive market, when it will turn you into one of the many buyers competing for your next home.

Our team has devoted a three-part series to tackle this conversation. What you're currently reading is Part One, and our goal is to lift the fog that is caused by all of the pressure and panic in the messaging you're hearing about the market right now. With that fog lifted, and with that pressure alleviated, it's possible you'll be able to make a sound decision about the right next step for you.

Before we discuss whether or not it's a good time for you to sell, let's establish the circumstances that are making this sellers market so hot:

Low interest rates have increased buyer demand. Interest rates continue to be (and will likely be for the next few years) historically low. Many first-time homebuyers are taking advantage of this opportunity, as well as individuals who want more and better house for the same money.

Appreciation potential is much greater on homes that are valued higher. Our market saw about 10% average appreciation between 2019 and 2020. If you own a home that was worth $150,000 in early 2019, this means the value appreciated $15,000 by early 2020. However, if you owned a home valued at $250,000, its value appreciated $25,000 in one year. That's a powerful thing, especially as low interest rates mean lower monthly payments.

My husband and I recognized this last summer. While we could have stayed in our Apple Valley home, we knew that we could leverage a lower interest rate to purchase a home with a higher value for the same money. Our monthly payment is almost identical, but the home we purchased was valued $40,000 higher than our home in AV, and this asset will perform better over time. Not to mention the lifestyle benefits of being in a home that has more style, better finishes, and in town-- we're very pleased.

Low inventory creates competition and stronger offers. We've talked about this a lot, but it's a powerful opportunity for sellers. Because demand is so high, and the number of homes available are so low, you have the opportunity to hand pick the contract with terms that work best for you. This leads to higher profits and faster sales.

But of course, you're savvy, and you already know all of this. And just because the market is hot, it doesn't necessarily mean that it's the right time for everyone to sell. If you're wanting to determine whether it's the right time for you to sell, here are some things to consider. This is important because there are good reasons and there are bad reasons to sell. Let's start with the good!

- You need to ask yourself if you enjoy the home you're in. If you're in the wrong location for your lifestyle, you should consider changing your location. Another great example of this is whether or not you need a home office (as many of us found ourselves without suitable spaces to work during the pandemic). Or, maybe you need more or less space. Whatever the reason, if the home you're in doesn't work, it doesn't work, and it's absolutely worth looking at a change.

- You want to upgrade your living situation. If you're inspired by my story, I want you to know this is absolutely possible for you. Especially if you purchased 3+ years ago, you should look at getting more and better house for the same monthly payment.

- You want to leverage the appreciation that the market is experiencing. This might feel a little risky, but can be a good decision based on your situation. I recommend discussing this thoroughly with your agent.

Now, for the bad reason...

Do not let anyone tell you that you should sell because you'll miss out on the strong seller's market. Making decisions out of panic will perpetuate more panic, and this kind of pressure will only serve to weaken your position. I am finding too many people in my community who are only considering selling because they feel like the housing bubble is about to burst at any moment. This just isn't the case, and we'll dive into why in part two!

For more valuable real estate content, check out our YouTube channel!

-Cassie Johnson, Key Realty - John Yoder Team

12

3 Tips to Help Buyers Emotionally Connect with Your Listing

3 Tips to Help Buyers Emotionally Connect with Your Listing

Just because buyer demand is high and buyer's have become more flexible in their search for a home, doesn't necessarily mean you should list your home as it is. In our team's experience, there are three very basic tips that will help take your listing to the next level to the people who matter most - your prospective buyer.Here's why this is important: If your listing has that wow factor and a buyer can emotionally connect with the property, your listing goes from "we can make this one work" to "we cannot miss out on this one." And the more buyers you can get to think this way about your listing, the stronger the offers will be, and you can hand pick the buyer with the best terms for you.Basically, the staging process is still turning out higher profits and faster sales for our clients.So, what are the most basic things you can do to make your home a "can't miss" in the eye of a buyer?

First, you want to make sure it is immaculately clean — sparkling, even. If the home feels, looks, and smells fresh, buyers will feel comfortable as they walk through the home. This includes pet odor. The biggest distraction for a buyer is a space that smells or feels dirty. This also happens to be one of the cheapest ways to bring your listing to the next level. If you're concerned about maintenance or about pet odor, you should speak with your agent about professionals who can help you along the way.

Second, you should replace family photos with neutral decor throughout the entire home. Why? Well, the entire idea of showings is getting the buyer to picture themselves in the property. If there are photos of you and your family everywhere, they will be distracted from this process. Let's make it easy for them and pack away everything that has your family's names or faces on it.I know this subject in particular can be a sensitive one. I understand this can be difficult because, for many of us, things like family photos are sentimental, treasured items that can bring comfort to us in our home. But remember, the marketing of the property is to make the home appealing to its next occupant. Still, if you're concerned about this, a simple compromise could be placing treasured family photos in a scrapbook that you can keep close by and peruse at your convenience.

Third, fresh paint can bring a major return on your sale. Picking neutral and calming colors throughout the home will make it more appealing to a wider pool of buyers without costing you an arm and a leg.Now, I've had countless conversations with clients in my staging experience, and the perspective of sellers often is "I want my home to feel lived in." And I get it. Most people aren't looking to walk through a home that's sterile and devoid of character. But again, if there's one perspective I would like to see shift in your mind through this video it's this:You're not necessarily trying to sell your home. You're trying to sell a buyer their future home. This is the approach that will pay off big time, every time.

If you're interested in learning more about the listing process, feel free to contact us today! For more helpful real estate content, visit our YouTube channel and subscribe!

-Cassie Johnson, Key Realty - John Yoder Team

|

|